Alkami Technology IPO analysis: Cloud software for bank digitization

The company is growing fast, but still burning cash

Alkami Technology provides an integrated one-stop solution for banks, that simplifies their operations and allows their customers to access digital banking solutions from any device. The company plans to go public on April 14th, and has raised $422 million since inception.

The company was founded by Gary Nelson, Sean McElroy, and Stephen Bohanon as iThryv on August 21, 2009, and later renamed to Alkami Technology. Alkami was founded as Gary Nelson asked Sean McElroy to review the code done by a development firm on an online banking solution. Sean found out that the company had done little valuable work and investors were duped1, and both of them decided to join up with Stephen Bohanon and formed Alkami.

Gary Nelson previously founded Advanced Financial Solutions, which was sold to Metavente.

Alkami’s Financial summary according to S-12:

Revenue of $112 million, up 53% YoY

151 clients

Net revenue retention of 117% in 2020 compared to 114% in 2019

Gross margin of 53% in 2020

Net loss of $51 million in 2020

Total addressable market (TAM) of $7 billion

Rule of 40 is only 16, based on revenue growth of 53% and free cash flow margin of -37%

No client represents more than 5% of revenue

Their main product is the Alkami Platform, which allows banks to onboard and engage with both retail and business clients. Alkami’s customers can augment the platform with upgrades from the company or from third parties through 220 extensions. Their solution is built on the cloud on top of AWS, so it’s a traditional SaaS company with recurring revenue. They also provide implementation services and custom development, which together comprise less than 7% of revenue.

At the end of 2020, they had 151 banks on the platform (up 28% yoy), which serve 9.7 million customers, with an additional 1.5 million under implementation. The aggregate assets of these banks were $222 billion in 2020.

Alkami usually targets banks with assets between $500 million to $100 billion. As a result, their solution is easily scalable and available for any bank. Smaller banks often do not have the technological capabilities to develop such a solution, instead they rely on up to 20 technology partners to run their back office, customer service functions and others. Alkami simplifies this under one roof.

Clients mostly start with one solution such as account opening or fraud protection and later extend it. Their customers use 9 of 26 of their modules, on average. Thanks to new product introductions, the 2020 cohort subscribed to 15 modules on average a 38% improvement over the 2019 cohort.

Alkami charges banks based on the number of registered clients that use their solution. The higher the number of users, the lower the per-seat price for a bank, which gives them incentives to market the software internally. According to the S-1 filing, Alkami’s clients grew the number of customers by 17% during last year, faster than the industry as a whole.

Banking for retail

Alkami’s retail solution offers great features, that many banks are still missing. Money movement functionality (bills, rent, transfers) is naturally a part of it. On top of that, their Financial wellness solution provides spending tracking and portfolio building, which helps their clients make wise financial decisions. In addition, banks gain unique insights based on spending habits, which they can use for targeted marketing.

It also includes personalized customer service features like chatbots and simplified verification to make the experience easy and smooth. Security is naturally a big part of it, and Alkami offers biometric and multifactor verification.

Banking for business

The business solution offers same-day ACH (automated clearing house) payments, advanced analytics for deep insights, automated billing and more.

What is Alkami’s value proposition?

Digital experience - consumers have gotten used to having everything fast, especially on mobile devices. Banking is one of industries, where account opening and many other fuctions can still be cumbersome and slow. In addition, mobile penetration in banking is growing and branch traffic is declining.

Regulation - constantly evolving, with a need to have a unified system to track compliance with local, national and international laws.

Low rates - pressure on banks to optimize and streamline their operations is significant, as the current low-rate environment squeezes their margins.

Complexity - banks use a mix of on-premise and cloud solutions, with dozens of vendors across back and front office.

Data aggregation - banks usually don’t have a unified view of the data used and stored in various systems. Alkami simplifies this and gives them

Cost - smaller institutions do not have the capital to compete with megabanks, which spend $25 billion on technology in 2019 alone. Alkami offers a solution that is affordable even for the smallest banks.

Speed of implementation - Alkami can deliver a new feature within a week, as was demonstrated during COVID last year with the skip-a-payment feature.

Sales and marketing

The sales cycles in banking are notoriously long and can last from 3 months to 12 months, with an additional 6 to 12 months for implementation. Their contracts have an average life of 70 months.

The company has achieved very strong retention rates and low churn: Since inception, of the 14 contracts that came up for renewal, 13 were renewed.

The company cites several successful case studies in their S-1 filing, where they were able to significantly increase deposits, loans, customer satisfaction and NPS scores at some of their clients.

How much does Alkami Technology earn?

The company achieved 53% growth during 2020, in partly also due to Covid, which forced some banks to digitize their operations quicker than might have been the case otherwise.

Gross margin expanded to 53% from 41% and operating loss narrowed to $35 million from $42.5 million a year before. Net loss was also impacted by a $15 million loss on financial instruments. The gross margin is similar to ther SaaS companies in the same space: Ncino (NCNO; 56%) and Q2 Holdings (QTWO, 43%). According to their S-1 filing, gross margins can get up to 70% once clients renew their contracts:

“Client renewals are also an important lever in driving our long-term gross margin targets, as we generally achieve approximately 70% gross margin upon renewal.”3

Cost of revenue includes hosting costs, direct cost of bill-pay, other third party software costs, client success team costs and others.

Sales and marketing costs increased 23% in 2020, slower growth due to savings on travel expenses ($0.8m) and the cancellation of their annual conference ($1.1m)

The net retention rate was 117% during 2020, and Alkami has steadily their ARR with existing clients according to their cohort analysis:

Alkami also calculates the Revenue per user metric (RPU), which is the ARR divided by the number of registered users at the end of a period. RPU grew from $10.29 in 2018 to $12.23 in 2019 and $13.22 in 2020.

They still generates negative operating cash flow, -$39 million in 2019 and -$38 million in 2020. This might not necessarily be bad, however I always invest only in businesses that are cash flow positive, or that are very close to breakeven. To me, positive cash flow is a sign that a business is viable and does not have to rely on external capital anymore.

The company plans to float 6 million shares at $23.5, which would give them a cash balance of $289 million, assuming preferred is converted. Total assets are expected to be $370 million after the offering.

Alkami has $25 million in long-term debt and $30 million in operating leases. In addition, there are $49 million in long-term purchase commitments related to services from third parties like hosting and other products.

Market size and growth potential

There are over 10,000 financial institutions in US, managing over $25 trillion in assets, with megabanks holding 37% of that. According to their S-1, 51% of accounts opened in the second quarter of 2020 were at megabanks.

The company estimates the size of their TAM to be $7 billion, with 185 million registered users that could potentially use their platform based on its current features. Their latest acquisition of ACH Alert LLC ($1 million revenue contribution in 2020) has helped them expand into online fraud prevention, increasing their TAM by $750 million according to the company. Digital banking penetration in US is 70% according to their S-1 filing, and Alkami expects a convergence towards 100% in the future.

According to Allied Market Research, the digital banking software market is expected to reach $11 billion by 2027, up from $4 billion in 2019, growing at a CAGR of 14%.4

Grow the number of users at existing clients - Alkami estimates that their penetration among clients is only 70%

New clients - Still a large and underserved market out there

Expand product portfolio - Alkami invested 40% of revenue in R&D during 2020

Select acquisitions - such as ACH Alert

Competition

Their main competitors are Ncino (NCNO), Fiserv (FISV), Q2 Holdings (QTWO), Temenos AG and Jack Henry and Associates (JKHY). Here is a comparison of their main competitors and their financials.

Alkami Technology is the smallest firm among their peers based on revenue. Ncino (NCNO) has the highest valuation at 35x sales, while others are growing slowly or even declining. Alkami has the second highest gross margin, and highest revenue growth. According to reports5, the company is seeking a valuation of $2 billion, which would be less than 20x sales, somewhere between NCNO and QTWO.

Valuation

Alkami has a higher cash burn rate, so a lower multiple than NCNO makes sense, however should the growth persist into 2021, they will be revalued higher probably in-line with Ncino, implying a valuation of $4 billion.

The industry is very crowded and it will be very hard to increase margins in the future, even though the company mentioned 70% gross margins on customer renewals. New features that they come up with will be probably very quickly copied by competitors, so the company has to constantly innovate to keep pace with the evolving industry.

Everything comes down to growth, if Alkami can continue growing at 40%, they could reach $600 million in revenues by 2025 and a potential valuation of $12 billion at 20x sales. That would still imply a CAGR of 43%, if they are priced at $2 billion at the IPO.

It’s worth keeping an eye on Alkami, as they might surprise on the upside. But for now, the low management stake, negative operating cash flow and significant competition are keeping me away.

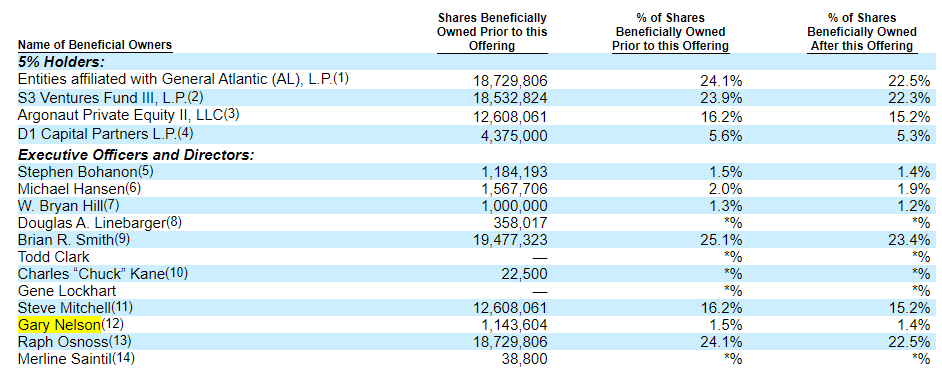

Shareholders

Largest shareholders after IPO are expected to be financial investors General Atlantic (22.5%), S3 Ventures (22.3%) and Argonaut private Equity (15.2%). Founders Stephen Bohanon and Gary Nelson own 1.4% each, which is pretty low. I like to invest in businesses where founders are still at the helm and own a sizeable stake, so this is something that puts me off a little bit.

There has been a lot of research done by Credit Suisse and Bain Capital on why family (owner-operator) companies outperform over the long run, so I always want to see management holding a significant share in the business.

Reviews

Alkami has a Glassdoor rating of 4.1 with a CEO approval rating of 88%. This is generally very good, and is probably also thanks to the equity compensation scheme that the company offers.

On Capterra, the Alkami platform has a rating of 3.5/5 based on only 2 reviews. Ncino has 4.75/5 based on 3 reviews6, which is a too small sample to draw any conclusions. On G2, the software review platform, Alkami has 1/5 based on only 1 rating7, and Ncino has 4.3 based on 11 ratings. Even though there are only a few reviews for each platform, Ncino seems to come out ahead.

Risks

Competition is very intense in this field, and Alkami does not have a unique selling point and their offering seems very similar to that of other players. Margin pressures are likely to be intense, as Ncino and Q2 Holdings target the same segment, while legacy players like Temenos and Fiserv are introducing their own offerings.

A Security breach could have a very negative impact on their brand name and customer retention. The company needs sophisticated technology to protect customer’s data from being accessed by hackers.

https://blog.seanmcelroy.com/2015/06/25/alkami-genesis/

https://www.sec.gov/Archives/edgar/data/0001529274/000119312521111300/d70489ds1a.htm

https://www.sec.gov/Archives/edgar/data/0001529274/000119312521111300/d70489ds1a.htm

https://www.alliedmarketresearch.com/digital-banking-platforms-market

https://www.pymnts.com/news/ipo/2021/bank-software-firm-alkami-plans-ipo-at-2b-valuation/

https://www.capterra.com/p/140944/nCino/

https://www.g2.com/products/alkami-banking-solutions/reviews